|

| Analyst Insight The GLP-1 RA market is transitioning from a demand-constrained to a supply-driven growth phase. As manufacturing capacity catches up with demand through 2026, the primary competitive battleground will shift from availability to access, meaning payer coverage breadth, patient affordability programs, and real-world adherence support will become the defining growth levers for market leaders. |

- Novo Nordisk's Ozempic & Wegovy: Semaglutide-based products from Novo Nordisk represent the most commercially successful GLP-1 products to date. Ozempic (semaglutide 0.5-2 mg weekly injection) held the largest single-product market share in 2025. In March 2024, Ozempic demonstrated a 24% reduction in risk of death and cardiac events in patients with type 2 diabetes and chronic kidney disease, expanding its label and driving physician adoption across nephrology and cardiology. Wegovy (semaglutide 2.4 mg weekly), approved for obesity in 2021, has shown mean weight losses of 15.8% at 68 weeks in clinical trials, making it one of the most effective non-surgical weight management interventions ever developed. Rybelsus (oral semaglutide, 14 mg once daily) completes the franchise as the first and currently only approved daily oral GLP-1 RA, primarily capturing T2DM patients with needle aversion; it achieved USD 2.8 billion in 2024 revenues and is undergoing clinical evaluation at higher doses (25 mg and 50 mg) for potential obesity approval.

- Eli Lilly's Mounjaro & Zepbound: Tirzepatide, a first-in-class dual GIP/GLP-1 receptor agonist, represents the next generation of incretin therapy. Marketed as Mounjaro for type 2 diabetes and Zepbound for obesity, it demonstrated superior weight loss outcomes up to 22.5% body weight reduction at 72 weeks, compared to semaglutide in head-to-head analyses. Commercially, tirzepatide's trajectory has been exceptional. From zero revenues pre-2022, Mounjaro generated USD 10.5 billion in 2024, while Zepbound (approved for obesity in November 2023) contributed USD 4.9 billion in its first full year, for a combined tirzepatide franchise revenue of USD 15.4 billion. By mid-2025, Lilly's GLP-1 revenues had surpassed those of Novo Nordisk for the first time, marking a historic market share inflection. In August 2024, Eli Lilly launched single-dose vials of Zepbound priced approximately 50% lower than existing versions, dramatically improving market accessibility. Concurrently, the company invested USD 1.8 billion in September 2024 to enhance GLP-1 manufacturing capacity to meet surging global demand.

- Eli Lilly's Orforglipron: Eli Lilly's orforglipron marks a strategic inflection point as the first truly oral, non-peptide small-molecule GLP-1 receptor agonist. Unlike Rybelsus, which requires fasting administration and has a narrow therapeutic window, orforglipron is a once-daily tablet requiring no fasting restriction, is manufactured via standard chemical synthesis (eliminating the complex biologics supply chain), and is projected to be significantly lower in cost of goods than peptide-based GLP-1 RAs. The Phase III ACHIEVE-1 trial (T2DM, June 2025) demonstrated statistically significant reductions in HbA1c across all doses versus placebo, with a safety profile consistent with injectable GLP-1 RAs. Topline results from the ATTAIN-1 and ATTAIN-2 trials (obesity) showed mean weight losses of 7.9–8.7% at 36 weeks, with dose-escalation data still maturing. Regulatory submissions are planned for 2025-2026, with a potential global launch in 2026-2027. The commercial implications of orforglipron approval would be far-reaching. Market access analyses project that oral administration could expand the eligible patient pool by 30-40% by capturing injection-averse patients and those in geographic areas with limited healthcare infrastructure for injectable drug administration. In emerging markets where cold-chain logistics constrain injectable GLP-1 RA distribution, orforglipron could unlock previously inaccessible patient populations in rural India, Southeast Asia, sub-Saharan Africa, and Latin America.

- Pipeline Entrants: Beyond the current Novo Nordisk-Eli Lilly duopoly, a robust pipeline of next-generation molecules is advancing toward commercialization. Amgen's MariTide (AMG133), a novel GLP-1 receptor agonist and GIPR antagonist delivered as a monthly subcutaneous injection, demonstrated up to 20% weight loss at 52 weeks in Phase II trials with notably sustained efficacy, a potential best-in-class durability profile. Phase III trials are underway across obesity, T2DM, and cardiovascular comorbidity indications. MariTide's monthly dosing schedule represents a meaningful convenience advantage versus weekly competitors and could command a pricing premium in markets where adherence is a challenge. In March 2025, Roche and Zealand Pharma announced a collaboration valued at up to USD 5.3 billion to co-develop petrelintide, a long-acting amylin analog, for overweight and obesity indications, both as monotherapy and in combination with GLP-1 RAs. This deal underscores the strategic importance of combination cardiometabolic regimens: petrelintide targets complementary pathways (satiety via amylin receptor agonism) that may produce additive weight loss and improved tolerability versus GLP-1 RA monotherapy. Novo Nordisk, AstraZeneca, and Viking Therapeutics are some of the other companies with products in the pipeline. The cumulative competitive pressure from these second-wave entrants is expected to accelerate pricing competition and innovation cycles across the therapeutic class through the 2027–2030 window.

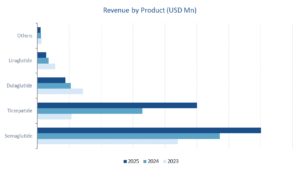

By Product

The product landscape of the GLP-1 receptor agonist market is dominated by two next-generation molecules, semaglutide and tirzepatide, which are rapidly displacing earlier-generation agents such as dulaglutide and liraglutide. Semaglutide retains market leadership with a 52.8% revenue share in 2025, having demonstrated robust clinical superiority data across the SUSTAIN, PIONEER, and STEP clinical trial programs. The growth is also underpinned by a broad portfolio spanning three distinct delivery formats and indication sets (Ozempic, Wegovy, Rybelsus), a deep and growing body of cardiovascular outcomes evidence, and Novo Nordisk's unmatched global commercial and distribution infrastructure across 170+ countries. The following chart details the product-wise revenue breakdown from 2023 through the forecast horizon.

By Application / Therapeutic Indication

Type 2 Diabetes Mellitus (T2DM) remains the dominant application segment, accounting for 81.2% share in 2025. The segment's growth is supported by the WHO's estimate that over 830 million individuals globally live with diabetes, with T2DM representing approximately 90-95% of all cases. GLP-1 RAs have become preferred agents in T2DM guidelines issued by the American Diabetes Association (ADA) and European Association for the Study of Diabetes (EASD), particularly for patients with established cardiovascular disease or high cardiovascular risk. This guideline-driven prescribing tailwind, combined with growing evidence that early initiation of GLP-1 RAs prevents progression from prediabetes to T2DM, is expected to sustain this segment's dominance through 2035, even as the obesity and cardiovascular segments grow faster in percentage terms. The Obesity / Chronic Weight Management segment is the fastest-growing application over the forecast years. The FDA's approval of Wegovy in 2021 and Zepbound in 2023 for chronic weight management marked a paradigm shift in the treatment of obesity, which affects over 1 billion people worldwide. The reclassification of obesity as a chronic disease by leading medical bodies has significantly improved reimbursement prospects globally. The pediatric obesity segment (FDA approved for adolescents ≥ 12 years in 2022 for Wegovy) represents an additional growth adjacency, with approximately 20 million adolescents in the U.S. clinically eligible. Cardiovascular Risk Reduction represents the emerging frontier forecasted to grow at a CAGR of approximately 32% through 2035. The approval of semaglutide for cardiovascular risk reduction (SELECT indication) in non-diabetic patients, alongside growing data on liraglutide (LEADER trial), is expected to catalyze this segment's expansion. By Route of Administration Injectable formulations dominated the GLP-1 receptor agonists market in 2025, driven by the once-weekly subcutaneous pen-injection format of Ozempic, Wegovy, Mounjaro, and Zepbound, which balances efficacy with patient convenience. However, oral GLP-1 RAs led by Rybelsus (oral semaglutide) are gaining traction among patients with needle phobia and those preferring daily oral regimens. The pipeline includes several oral candidates in late-stage development, including oral tirzepatide, which could substantially reshape the route-of-administration mix by the end of the forecast period. Oral GLP-1 RAs currently represent approximately 8% of total market revenues, primarily through Rybelsus (oral semaglutide). Growth of the oral segment is constrained by the pharmacokinetic challenges of peptide-based oral delivery (requiring specific fasting conditions and having bioavailability of only 1%), the modest weight loss outcomes versus injectable semaglutide, and the availability of superior injectable alternatives. However, the oral segment is the highest CAGR sub-segment on a forward-looking basis. The anticipated approval of orforglipron, which circumvents the oral peptide delivery limitations through its small-molecule design, is expected to create an inflection point in oral segment growth from 2027 onward. Projections suggest the oral segment could capture 25-35% of market revenues by 2035, fundamentally reshaping the delivery format mix.By Distribution Channel

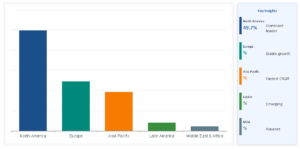

Retail pharmacies remain the primary distribution channel in 2025, while online pharmacies represent the fastest-growing channel, driven by the rapid expansion of telehealth platforms and compounding pharmacies, particularly in the U.S., which fill demand gaps during shortage periods. Regulatory crackdowns on compounded GLP-1 Ras, following FDA guidance, are expected to redirect patients toward branded pharmacy channels through 2026-2027. Online pharmacies and direct-to-consumer (DTC) telehealth platforms represent the fastest-growing distribution channel, expanding at a significant CAGR from 2026 to 2035. Platforms such as Ro, Hims & Hers, Found, and WeightWatchers Clinic have built vertically integrated models combining telehealth prescribing, pharmacy fulfillment, and digital adherence coaching, capturing an estimated 8-12% of total U.S. GLP-1 RA prescriptions by mid-2025. Following the FDA's crackdown on compounding pharmacies for semaglutide and tirzepatide (shortage designation lifted in 2025), several of these DTC platforms transitioned to branded product dispensing, creating a new, high-growth branded channel for manufacturers. Hospital and institutional pharmacies account for a smaller share of GLP-1 RA distribution but are growing as hospital-based obesity medicine programs and endocrinology clinics expand their patient management volumes. Regional Insights GLP-1 Receptor Agonist Market Share by Region (USD Million), 2025

North America

North America commands a dominant 75.5% share of the global GLP-1 RA market in 2025, underpinned by the highest per-capita healthcare spending, robust insurance reimbursement infrastructure, and high obesity prevalence (approximately 42% in the U.S. adult population). The U.S. alone accounts for the majority of North America revenues, with Ozempic consistently ranked as one of the most prescribed branded medications by value. The combination of semaglutide and tirzepatide product launches, coupled with expanding Medicare and commercial payer coverage under obesity benefit riders, cements the region's leadership position through the forecast period. The passage of the Treat and Reduce Obesity Act (if enacted) and the Biden/Trump-era Inflation Reduction Act drug pricing provisions will have material implications for GLP-1 RA market dynamics in the U.S. The IRA's Medicare drug price negotiation mechanism, which selected the first 10 drugs for negotiation in 2023, is not expected to include GLP-1 RAs in the near term, given their recent launch dates, but the broader pricing pressure dynamic and the precedent of government negotiation create uncertainty for long-term U.S. pricing assumptions.Europe

Europe is the second-largest market, with Germany, the UK, and France constituting the largest country markets. Semaglutide products dominate, particularly given Novo Nordisk's home market advantage and strong EMEA commercial infrastructure. HTA-related pricing pressures and reimbursement restrictions, particularly in France and Italy, temper growth relative to the U.S. However, the progressive recognition of obesity as a chronic disease and improving payer policies are expected to drive a re-acceleration in European adoption through 2027-2030. The Nordic countries present a particularly high per-capita utilization profile, reflecting both higher average healthcare expenditures and Novo Nordisk's country-specific brand strength. Denmark alone accounts for a disproportionate share of European GLP-1 RA revenues on a per-capita basis. Southern and Eastern European markets remain significantly underpenetrated relative to GDP-adjusted disease burden, constrained by lower per-capita healthcare budgets and less favorable reimbursement conditions. Progressive HTA framework harmonization under the EU HTA Regulation (effective January 2025) is expected to streamline multi-country reimbursement decisions and potentially accelerate European market access for future GLP-1 RA approvals.Asia Pacific

Asia Pacific represents the highest-growth opportunity region, expanding at a CAGR of approximately 15%. Japan is the region's largest market, supported by early regulatory approvals and strong diabetes infrastructure. The Japanese Pharmaceuticals and Medical Devices Agency (PMDA) approved Ozempic in 2021 and Wegovy in 2023, with tirzepatide (Mounjaro) approved in 2023 for T2DM. China is the fastest-growing country, with semaglutide achieving rapid adoption following its 2022 China approval. India represents a significant nascent opportunity, currently, but is expected to scale considerably given the country's 77 million diabetic population and increasing middle-class healthcare spending. The development of locally manufactured, lower-cost semaglutide products by Indian generics manufacturers (Sun Pharma, Cipla, and Dr. Reddy's have all announced GLP-1 RA development programs) is expected to expand market access in the 2027–2032 timeframe materially.Latin America & Middle East/Africa

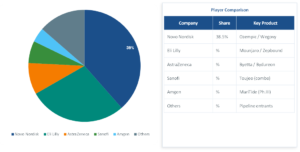

Latin America GLP-1 RA market is characterized by a high disease burden but constrained by affordability and reimbursement limitations. Market access is gradually improving through government health programs and private insurer expansion. Novo Nordisk and Eli Lilly have both made direct investment commitments to Latam commercial infrastructure, including dedicated medical affairs teams, patient support programs, and partnerships with local pharmacy chains to expand GLP-1 RA distribution coverage. The Middle East & Africa GLP-1 RA market is led by Saudi Arabia and the UAE, where strong healthcare infrastructure and high prevalence of cardiometabolic risk factors drive adoption. Both regions are expected to record above-average CAGRs through 2035 as market access expands. Both Ozempic and Wegovy are reimbursed in Saudi Arabia and the UAE for their approved indications, with tirzepatide gaining approval and market access in both countries through 2024. Sub-Saharan Africa represents a long-term strategic opportunity that remains effectively nascent from a commercial GLP-1 RA perspective. South Africa is the exception within the region, with a more developed private healthcare sector and an established specialty pharmacy network enabling limited branded GLP-1 RA access for insured patients. Competitive Landscape The global GLP-1 receptor agonist market exhibits a highly concentrated competitive structure, with two pharmaceutical giants, Novo Nordisk A/S and Eli Lilly and Company, collectively controlling over the majority of total market revenues in 2025. Significant barriers to entry, including complex biologics manufacturing, extensive clinical trial requirements, established brand equity, and entrenched physician relationships, reinforce this duopolistic dynamic. GLP-1 Receptor Agonist Competitive Market Share, 2025

Novo Nordisk A/S

Novo Nordisk has achieved a position of unrivaled dominance in the GLP-1 RA space, with semaglutide products generating a global revenue of approximately USD 28.1 billion in 2024, equivalent to over 80% of the company's total pharmaceutical revenues. The company's competitive moat rests on its proprietary semaglutide molecule chemistry (fatty acid acylation enabling extended half-life), first-mover advantage in once-weekly injectable and oral GLP-1 formulations, and robust EMEA/US commercial infrastructure. Novo Nordisk's pipeline includes oral semaglutide (higher dose) for obesity, amycretin (GLP-1/amylin dual agonist), and semaglutide label expansions into CKD, NASH/MASH, and MACE reduction. The company has committed USD 6.7 billion to manufacturing capacity expansion through 2026, including a major facility acquisition in the U.S.Eli Lilly and Company

Eli Lilly has emerged as Novo Nordisk's most formidable competitor following the blockbuster launches of Mounjaro (tirzepatide for T2DM, approved 2022) and Zepbound (tirzepatide for obesity, approved 2023). Tirzepatide's dual mechanism action on both GIP and GLP-1 receptors delivers superior clinical outcomes, including up to 22.5% average weight loss in SURMOUNT-1 trial versus ~15% for semaglutide in STEP trials, positioning it as the therapy of choice for weight management in clinical practice. Eli Lilly's pipeline further includes retatrutide (GIP/GLP-1/glucagon triple agonist, Phase III) and oral tirzepatide, which could unlock substantially larger patient populations averse to injectable delivery. Lilly's projected 2025 GLP-1 revenues of USD 29.4 billion mark a trajectory to potentially surpass Novo Nordisk in total GLP-1 revenues within the forecast period.Competitive Pipeline & Emerging Players

Beyond the current duopoly, the competitive pipeline is expanding significantly. Notable late-stage candidates include: orforglipron (Eli Lilly, oral non-peptide GLP-1 agonist, Phase III); cagrilintide/semaglutide combination (Novo Nordisk, Phase III); pemvidutide (Altimmune, GLP-1/glucagon, Phase II); and several oral small-molecule GLP-1 agonists from Pfizer, Roche, and AstraZeneca. Biosimilar semaglutide entrants are expected post-2028 as key patents begin expiring, though brand loyalty, delivery device patents, and manufacturing complexity may delay significant market share erosion.| Key Strategic Takeaway: The GLP-1 RA market is at an inflection point, transitioning from a diabetes-centric specialty drug class to a broad cardiometabolic franchise. Companies with diversified GLP-1 portfolios spanning multiple indications, delivery formats including injectable & oral, and geographies are best positioned to capture the multi-billion dollar opportunity projected through 2035. Pipeline innovation, manufacturing scale, and reimbursement access are expected to define the competitive battlegrounds over the next decade. The anticipated entry of biosimilar competitors beginning around 2028 is expected to introduce significant pricing pressures across the market. In response, leading companies will need to adopt proactive strategies such as expanding therapeutic indications, investing in advanced drug delivery and device innovations, and strengthening patient engagement and loyalty programs. These measures will be critical for sustaining market share, reinforcing brand differentiation, and maintaining revenue growth in an increasingly competitive landscape. |

| Coverage | Details |

| Base Year | 2025 |

| Actual Data | 2021-2025 |

| Forecast Years | 2026-2035 |

| Unit and Growth Rate (CAGR) | Revenue (USD Million/Billion) and CAGR from 2026 to 2035 |

| Geographic Scope | ● North America: U.S., Canada, Mexico ● Europe: UK, Germany, France, Italy, Spain, Russia, Denmark, Sweden, Norway ● Asia Pacific: Japan, China, India, Australia, South Korea, Thailand, Singapore ● Latin America: Brazil, Argentina ● MEA: South Africa, Saudi Arabia, UAE |

| Segment Scope | ● Product ○ Semaglutide (Ozempic, Wegovy, Rybelsus), ○ Tirzepatide (Mounjaro, Zepbound) ○ Dulaglutide (Trulicity) ○ Liraglutide (Victoza, Saxenda) ○ Others ● Application ○ Type 2 Diabetes Mellitus ○ Obesity / Chronic Weight Management ○ Cardiovascular Risk ● Route of Administration ○ Injectable / Parenteral ○ Oral ● Distribution Channel ○ Hospital Pharmacies ○ Retail Pharmacies ○ Online Pharmacies |

| Companies Covered | ● Eli Lilly and Company ● Sanofi ● Novo Nordisk A/S ● AstraZeneca ● Teva Pharmaceutical Industries Ltd. ● Glenmark Pharmaceuticals ● Emerging Companies (Pipeline Products) |

This report addresses

Table of contents will appear here once uploaded in Pods (table_of_contents field).

How fragmented evidence becomes a figure you can defend in a boardroom.

A market number is a claim about the world. For that claim to hold up in an investment committee, a strategy review, or a regulatory submission, it has to be traceable, corroborated, and reproducible, not the output of one model or one source. What follows is the discipline behind every Databeta healthcare estimate: how the market is built from the ground up, how it is checked from the top down, and how the two are reconciled before a single figure is published.

Building the market from its smallest measurable unit

Bottom-up is the method we lead with. It constructs a market from the unit that can actually be counted, whether that is a patient, a procedure, or an installed device, and works upward to total addressable revenue. Because each input is gathered separately, the model stays transparent: any number can be opened up and questioned down to the assumption that produced it. Which of the two approaches below we use depends on whether demand is anchored in a disease or in a device.

Approach A · Epidemiological ModellingFor pharmaceutical, biotech, and diagnostics markets, demand traces back to disease. That lets us size a market from the patient population downward rather than inferring it from revenue alone. Each stage in the chain below is its own research question with its own evidence. Population figures come from epidemiological literature and bodies such as the WHO, IDF, CDC, UNAIDS, and national registries. Diagnosis and treatment rates, often the single biggest gap between a large theoretical market and a small real one, come from treating clinicians in primary interviews and are cross-checked against claims data. Therapy share and net price are assembled from payer and manufacturer inputs.

Worked example Oncology molecular diagnostics ▾

We start with incident cancer cases for each geography, then apply the share proceeding to molecular biomarker testing, drawn from oncologist interviews and pathology laboratory throughput. We layer in platform share and the reimbursed net price, arriving at addressable revenue for each modality in each country.

= $620M addressable revenue (US, NGS modality, 2025)

The build is then aggregated across modalities and geographies and reconciled against the disclosed revenues of the major IVD players. Where the aggregated build and the disclosed revenues disagree, the gap is investigated before anything is published.

Approach B · Volume Build-Up

When epidemiology alone does not resolve to revenue, because the product is a device, a consumable, or a service rather than a therapy, we build from unit economics instead. This is the standard for medtech, sexual wellness, and clinical outsourcing markets. Procedure and unit volumes come from hospital discharge databases, insurance claims, and device registries. Average selling price is assembled from distributor interviews, tender disclosures, and manufacturer pricing intelligence. For clinical trials and outsourcing work, the unit becomes the trial or project, and revenue per unit is derived from CRO rate cards and sponsor budget benchmarks validated through primary research.

Worked example Glucose monitoring consumables ▾

We take the diagnosed, self-monitoring patient population and apply average annual test-strip consumption per user, sourced from diabetes nurse interviews and pharmacy offtake data. We then multiply by net ASP after channel discounting.

= segment revenue, cross-checked against distributor sell-through

Because consumption intensity varies widely by market and payer, the per-user figure is built separately for each geography rather than applied as a global average.

Challenging the build from a known parent market

Top-down starts from a parent market that is already defensible, such as total pharmaceutical spend, total diagnostic testing revenue, or total digital health expenditure, and apportions it by penetration, segment share, and geography. Its job is not to replace the bottom-up build but to test it. Before any numbers are run, we fix three nested boundaries that decide exactly what is being measured and what is deliberately left out.

Approach A · Secondary Research and Market Share

Publicly reported revenues of the leading players are aggregated and cross-referenced to estimate total category size. Share splits are validated against earnings calls, regulatory filings, licensed databases, and trade publications. In a market where three or four dominant players disclose their revenues, this method alone can bracket the total tightly.

Worked example Enterprise healthcare IT ▾

For a segment where four enterprise vendors account for most of the revenue, we aggregate disclosed and estimated revenues, then apply a coverage factor for the smaller unlisted players, derived from channel-partner interviews.

= total category size, then tested against the bottom-up build

The result is never taken on its own. It becomes one side of the triangulation described in section 03.

Approach B · Growth-Rate Triangulation

Historical CAGR is benchmarked across several independent data points, including company revenue trajectories, procedure-volume trends, and claims data, then adjusted for the demand-side forces that will move the market: demographic shifts, improving diagnosis rates, widening access, and regulatory catalysts. We do not apply a single blended rate. Every driver is modelled as its own quantified contribution, so the forecast can be stress-tested one assumption at a time.

Worked example Biotech cell therapy CAGR ▾

The base-case growth rate is assembled from three inputs, each modelled on its own: the pace of new indication approvals widening the eligible patient pool, the rate at which reimbursement coverage expands across payer classes, and manufacturing yield improvements that lower cost of goods and open access to broader populations.

= 9.3% base-case CAGR (range 6.1% to 13.7%)

Conservative, base, and optimistic cases are run for each driver rather than for the blended total, so a change in any single assumption can be traced through to the forecast.

What it means when the two methods disagree

When the bottom-up and top-down estimates land close together, confidence is high. When they diverge, we do not split the difference. The gap is investigated, because in healthcare markets a divergence almost always points to one specific, fixable cause. A targeted round of follow-up interviews with clinicians, payers, or distributors resolves the discrepancy at its source, and the reconciled figure is the one that gets published.

No figure is published until both methods have been run, reconciled, and independently reviewed. What makes a Databeta number defensible is not the sophistication of any one model. It is the discipline of the process: two independent builds, an honest reckoning with where they disagree, and a resolution traced back to primary evidence.